- 1.Introduction to Digital Rupee and Policy Thereof.

- 2.How the Food Subsidy Pilot Works

- 3.The Importance of This to the Financial System of India.

- 4.Impact on Households and Everyday Financial Behavior

- 5.Transparency, Governance and Fiscal Efficiency.

- 6.Challenges and Risks to Address

- 7.The Bigger Picture: India’s CBDC Strategy

- 8.What This Signals for the Future of Banking and Payments

India has made a significant step in the way of implementing the digital currency of central banks into the sphere of real welfare. In a report by CNBC-TV18, the government has introduced a pilot on the digital rupee which was used to deliver food subsidies on the Pradhan Mantri Garib Kalyan Anna Yojana. This evolution marks a new stage in the process of evolution of digital payments in India, but it is no longer a retail pilot but a direct benefit transfer covering a sovereign digital currency.

The program is based on the years of preparation done by the Government of India and the Reserve Bank of India to digitalize the payments and limit the opportunities of leakages in the delivery of subsidies. Since India is becoming a global powerhouse in fintech creation, the digital rupee pilot is a tactical fusion of the monetary policy, welfare reform, and digital infrastructure.

Introduction to Digital Rupee and Policy Thereof.

The Indian one is the digital rupee, a digital version of central bank digital currency (CBDC), or the sovereign digital money issued and controlled by the central bank. However, in contrast to cryptocurrencies, CBDCs are issued currency with state support and, therefore, have the security of any other fiat currency and the performance of online payments.

Since 2022, the RBI has been conducting wholesale and retail CBDC pilots. The early retail trials were dedicated to person-to-person payments, merchant payments and closed groups of users. The food subsidy pilot is a shift towards government disbursements, which is one of the most influential applications of CBDCs in the world.

The world has seen nations like China adopt the digital yuan and European Central Bank consider the digital euro that has added welfare distribution to the list of reasons through which CBDC can be adopted. The behavior of India is unique since the country has already a well-developed digital payment infrastructure that is supported by UPI, Aadhaar, and direct benefit transfers.

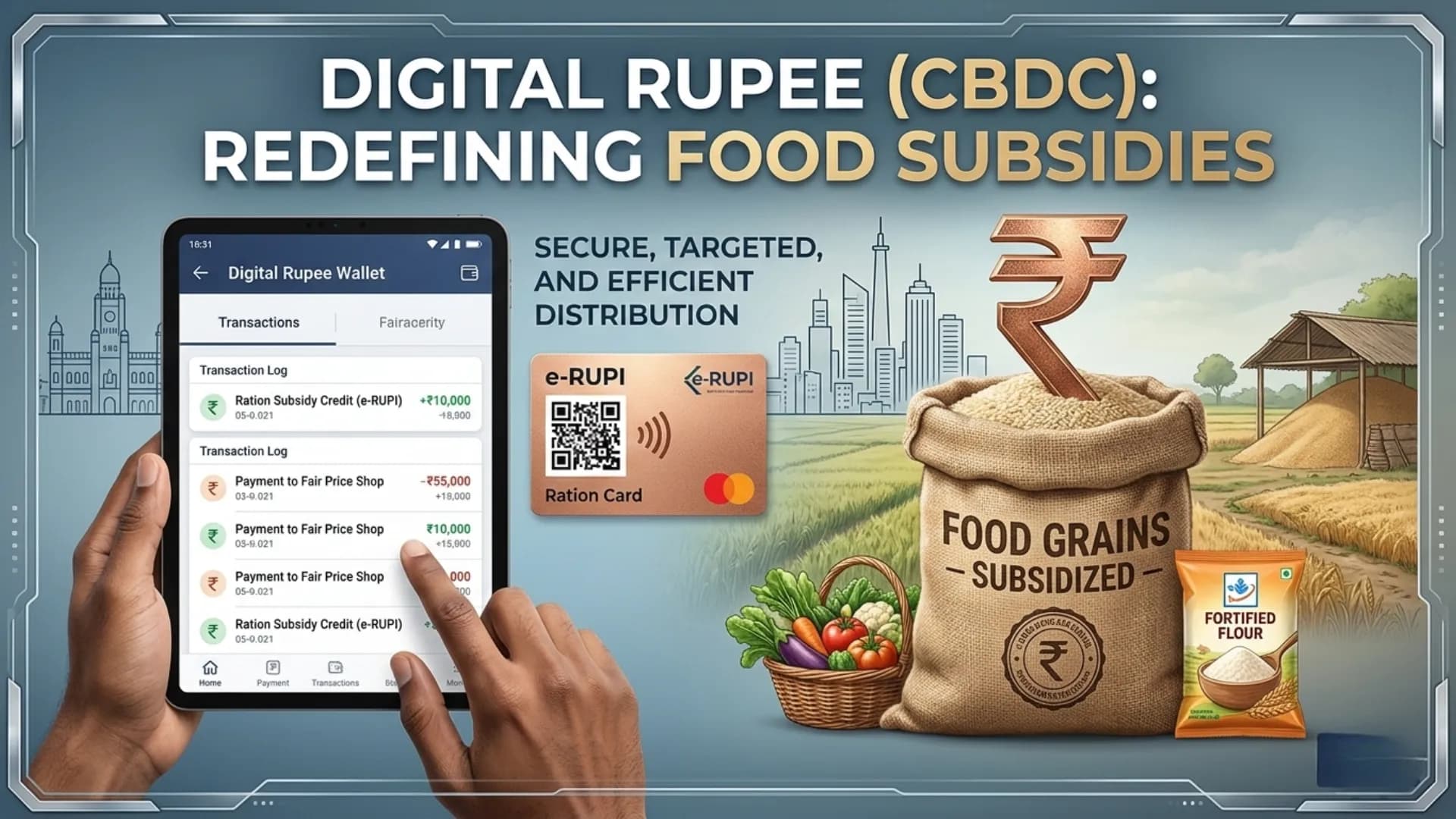

How the Food Subsidy Pilot Works

The pilot has changed the food subsidies which were delivered under traditional systems of food distribution or bank transfers to be channeled through digital rupee wallets. The entitlements are given to the beneficiaries in the form of digital currency which in turn can be utilized within the authorized ecosystem to buy food grains or other essentials.

The model minimizes intermediaries on subsidy flows and also adds programmability to it - a characteristic of CBDCs. Programmable money will enable the authorities to make sure the money that is used is disbursed to the purpose like buying food instead of being redirected to other activities.

This is especially applicable to programs such as the Garib Kalyan Anna Yojana, which helps millions of families by giving them subsidized food. The digitization of this pipeline will be more transparent and auditable.

The Importance of This to the Financial System of India.

The pilot highlights the ambition of India, which is to redefine the provision of public finance. Provided successful scaled, CBDC-based welfare transfer would transform the way subsidies were structured, with fewer administrative costs, and no ghost beneficiaries.

India already administers the largest direct benefit transfer system in the world, which has saved some 2 lakh crore (more than 24 billion) in terms of leakages since it was started. The incorporation of CBDCs may simplify this ecosystem further because it allows the settlement and traceability in real-time.

This is a disruption and an opportunity to the banks and other payment providers. Although in certain transactions, CBDCs may eliminate intermediaries, the financial institutions will likely continue to dominate the distribution of the wallets, onboarding and infrastructural support.

Impact on Households and Everyday Financial Behavior

The change in the use and access of subsidies will be the most immediate. The recipients will have a more direct relationship with digital wallets instead of the ration system or bank-tied transfer. This could help speed up the digitalization of semi-urban and rural regions in the same way that UPI increased financial inclusion.

Purchasable subsidies would make sure that the welfare funds are utilized more effectively. An example of this is the digital rupee-based entitlements which can only be utilized at specific stores and they can limit abuse without hindering the basic necessities.

Accessibility will however be important. The simplicity of interfaces, offline support, and multilingualism will be the key factors defining the ease with which the beneficiaries will be integrated into digital currency-based systems. The experience that India has had with Aadhaar-based payments indicates that education and grievance redress systems should be implemented to users.

Transparency, Governance and Fiscal Efficiency.

Governance The implementation of a CBDC-based welfare delivery presents unparalleled transparency. All transactions are logged in a controlled ledger environment, and subsidy flows can be tracked almost in real-time.

This can enhance fiscal planning as policymakers will have a detailed information on utilization patterns. As an example, the government may monitor the speed of the spending of the subsidies, demand patterns in the regions, and seasonal fluctuations in the consumption.

This kind of data-driven information can be used to redesign welfare programs in order to be more targeted. The dynamic subsidy models may develop over time and they may be in the form of allocations which automatically changes in response to either economic indicators or regional needs.

Challenges and Risks to Address

Despite the promise, several challenges remain. Digital literacy gaps could create initial friction in adoption, especially among older populations or those unfamiliar with smartphones. Ensuring offline usability and assisted payment models will be critical.

Privacy concerns are another consideration. While CBDCs provide traceability, maintaining a balance between transparency and individual data protection will be vital to public trust. Regulatory clarity around data usage and safeguards will play a defining role.

Infrastructure readiness also matters. Reliable internet connectivity, secure wallet solutions, and scalable backend systems will determine whether pilots can transition into nationwide rollouts.

The Bigger Picture: India’s CBDC Strategy

The food subsidy pilot is not an isolated experiment but part of a broader roadmap. India is exploring CBDC use cases across wholesale settlements, cross-border payments, and retail transactions.

In the long term, digital rupee adoption could strengthen monetary policy transmission, reduce cash management costs, and enhance financial resilience. For example, CBDCs could enable faster stimulus disbursements during economic shocks or natural disasters.

India’s digital public infrastructure — widely recognized as one of the most advanced globally — provides a strong foundation for scaling CBDCs. The integration of identity, payments, and banking rails gives India a structural advantage over many economies still building foundational systems.

What This Signals for the Future of Banking and Payments

Pilot programs The digital rupee is an indication of a transition to programmable finance, money with rules and logic embedded in it. This may affect the way governments in the global arena reconsider the delivery of welfare, taxation, and expenditure by the government.

In the case of financial institutions, one of them will be the adjustment to a hybrid ecosystem, where the cash, bank deposit, and CBDC are all present. There could be new business models of wallet services, digital custody and fintech value add solutions.

In the meantime, payment innovation will be quickened. CBDCs might supplement other preexisting rails such as UPI, allowing new transaction categories such as conditional payments, automated subsidies, and real-time monitoring of public finances.

Conclusion

The transition by India to experiment with food subsidies in the form of digital rupee is a turning point in the history of the digital adoption of currency. The combination of welfare provision and CBDC infrastructure is an experiment that the country could transform the definition of both public finance and daily financial transactions.

When implemented properly, this initiative may improve the transparency, minimize leakages, and update the methods of subsidies delivery. Meanwhile, its implementation will have to be thoughtful, well-tuned and inclusive.

Its results will not just define the future of sovereign digital money in India, but also provide lessons to policymakers and central banks around the world who may consider the future of sovereign digital money.

Grow your business with Go Finance- take quick, easy finance and business loans specially tailored to your growth. We offer any kind of finance and loan at no problematic implementation.